Hey there, fellow American navigating the wild world of health insurance. If you’re staring at your computer screen thinking, “Why does this feel like trying to decode ancient hieroglyphics while juggling bills?”—you’re not alone. In 2026, health insurance isn’t just paperwork; it’s your safety net against that random ER visit that could otherwise turn your savings account into a ghost town. This guide cuts through the jargon with real talk, a dash of humor (because laughing beats crying over deductibles), and straight-up rankings based on the latest data. We’ll cover everything from basic ABCs to top picks for families, seniors, and solo folks. By the end, you’ll feel like a pro who can actually compare plans without a headache. Let’s dive in—no fluff, just facts with a smile.

Understanding the Basics of Health Insurance in 2026

Health insurance in the USA is basically a group bet: you pay monthly premiums so that when life throws a curveball—like a broken arm from slipping on ice or a surprise appendicitis—you’re not left footing the entire bill yourself. In 2026, things have shifted a bit since the enhanced subsidies from the pandemic era fully expired at the end of 2025. That means premiums after tax credits are averaging around $50 a month for the lowest-cost plans on HealthCare.gov for eligible folks, which is still a steal compared to pre-2020 days but a tad higher than last year.

Don’t worry if that sounds confusing—we’ll break it down. Your plan covers “essential health benefits” like doctor visits, hospital stays, prescriptions, mental health, and preventive care (think free annual check-ups and vaccines). But not all plans are created equal. Premiums are what you pay every month to keep the policy active. Deductibles are the amount you shell out before insurance kicks in big-time. Copays and coinsurance? Those are your share of costs after the deductible—usually a flat fee or percentage.

Humor break: Imagine health insurance as a gym membership you actually use. You pay upfront hoping you won’t need it much, but when that “injury” (cough, couch potato life) hits, you’re glad you didn’t cancel. In 2026, with inflation and medical costs still climbing, skipping coverage is like playing Russian roulette with your wallet. About 95% of folks on the marketplace now have three or more insurers to choose from, so competition is keeping things somewhat sane.

Key 2026 twist: All Bronze and Catastrophic plans are now eligible for Health Savings Accounts (HSAs). That means you can sock away pre-tax dollars for medical expenses, like a secret piggy bank for future doctor bills. It’s a game-changer for healthy people who want lower premiums and tax perks.

Types of Health Insurance Plans: Pick Your Adventure

Not every plan feels the same when you need care. Here’s the lineup, explained like you’re chatting with a buddy over coffee.

- HMO (Health Maintenance Organization): These are like the budget-friendly tight-knit family. You pick a primary care doctor who coordinates everything. Cheap premiums, but you usually stick to in-network providers and need referrals for specialists. Great if you hate paperwork and love one-stop shopping.

- PPO (Preferred Provider Organization): The flexible crowd-pleaser. Higher premiums, but you can see out-of-network docs (for more cash out of pocket) without referrals. Perfect for travelers or folks with favorite specialists across town.

- EPO (Exclusive Provider Organization): A hybrid—PPO vibes but no out-of-network coverage except emergencies. Lower costs than full PPOs, but you’re locked into the network.

- POS (Point of Service): Like an HMO with PPO upgrades. Referrals needed for in-network, but out-of-network is an option (at a price).

- High-Deductible Health Plans (HDHPs): These pair with HSAs and have sky-high deductibles but rock-bottom premiums. Ideal for young, healthy people who rarely see doctors. In 2026, they’re even more popular thanks to those new HSA rules.

- Catastrophic Plans: Only for under-30s or those with hardships. Super cheap premiums, massive deductibles, but they cover big emergencies after you hit the out-of-pocket max.

Lists make this easier, right? Here’s a quick pros/cons table for the big ones:

| Plan Type | Pros | Cons | Best For |

|---|---|---|---|

| HMO | Low premiums, coordinated care | Limited network, referrals required | Budget-conscious families with local docs |

| PPO | Flexible network, no referrals | Higher premiums and deductibles | People who travel or need specialists |

| EPO | Balanced cost and flexibility | No out-of-network (mostly) | Those wanting PPO perks without the price |

| HDHP + HSA | Lowest premiums, tax savings | High upfront costs | Healthy young adults or self-employed |

How the ACA Marketplace Works in 2026: Your Government-Sponsored Shopping Mall

The Affordable Care Act (ACA, or Obamacare) marketplace is where most individuals and families shop for private plans. In 2026, open enrollment for the year wrapped up in January, but special enrollment periods still exist for life changes like job loss or marriage. HealthCare.gov serves 30+ states, with others running their own (like New York or California).

Big 2026 update: No more year-round enrollment for most folks. You’ve got to hit the window or qualify for a special trigger. Subsidies are still there based on income (100-400% of federal poverty level), but the extra boosts from recent years are gone, so some people are paying more out of pocket.

Metal tiers label the plans like Olympic medals:

- Bronze: 60% covered by insurance (you pay 40%). Cheapest premiums, highest out-of-pocket.

- Silver: 70% covered. Best value for many, especially with cost-sharing reductions if your income qualifies.

- Gold: 80% covered. Higher premiums, lower deductibles—great for frequent doctor-goers.

- Platinum: 90% covered. Pricey but you barely pay when sick.

Average unsubsidized premiums hover around $590/month nationally, but subsidies slash that dramatically for many. Plans must cover pre-existing conditions—no more denials for that old soccer injury.

Pro tip: Use the marketplace’s plan preview tool. It’s like test-driving cars but for insurance. Enter your ZIP, income, and meds, and it spits out personalized options.

Top Health Insurance Companies Ranked for 2026

Alright, the main event: rankings. We pulled from sources like Forbes Advisor, Insure.com, and others analyzing premiums, complaints, networks, and customer feedback for 2026 ACA plans. Kaiser Permanente takes the crown again—six years running in some surveys—for blending low costs with top-notch care.

Here’s a simple comparison table of the heavy hitters (based on average Silver plan data for a 40-year-old, unsubsidized):

| Rank | Company | Best For | Avg. Monthly Premium | Silver Deductible | Key Strength | Availability |

|---|---|---|---|---|---|---|

| 1 | Kaiser Permanente | Overall value & integrated care | ~$498 | ~$4,115 | Low complaints, seamless doctor-pharmacy setup | 8 states + DC |

| 2 | Blue Cross Blue Shield | Nationwide network | ~$654 | ~$4,319 | Huge provider list (1.7M+), flexible plans | All 50 states |

| 3 | Aetna (CVS Health) | Low complaints & perks | ~$606 | ~$3,586 | CVS discounts, solid deductibles | 17 states |

| 4 | Humana | Medicare crossover & satisfaction | Varies | Varies | Strong in surveys | Widespread |

| 5 | UnitedHealthcare | Employer & global options | Higher | Competitive | Big network, tech tools | National |

Blue Cross Blue Shield affiliates (like BCBS of Michigan or Florida Blue) win for sheer size. Need a specialist in rural Alaska? Probably covered. They offer every metal tier and plan type. Premiums run higher, but peace of mind is priceless. Funny story: One guy switched to BCBS and joked his “network” now includes every doctor he’s ever heard of.

Aetna gets props for the fewest gripes. Own a CVS card? You score extra discounts. Great for urban folks who want reliable claims processing.

Other notables: Molina for low-income families with rock-bottom complaints, Oscar for tech-savvy users with app-first vibes, and Cigna for extras like mental health apps. UnitedHealthcare dominates employer plans but can feel corporate and bureaucratic—think “big box store” vs. Kaiser’s “boutique clinic.”

For families, BCBS often edges out due to kid-friendly networks. Self-employed? Kaiser or Aetna if available in your state.

Best Plans for Individuals and Families

Solo? Grab a Bronze HDHP if you’re under 40 and healthy—premiums as low as $350-400/month in many spots. Families of four? Silver is the sweet spot; subsidies can drop costs to under $100/month combined for many. Look for plans with pediatric dental and vision baked in (ACA requirement).

Real example: A 35-year-old in California with Kaiser might pay $442 for Silver and enjoy zero-hassle virtual visits. Same person in New York with Empire (BCBS) gets more network choices but slightly higher deductibles. Always run the numbers on Healthcare.gov.

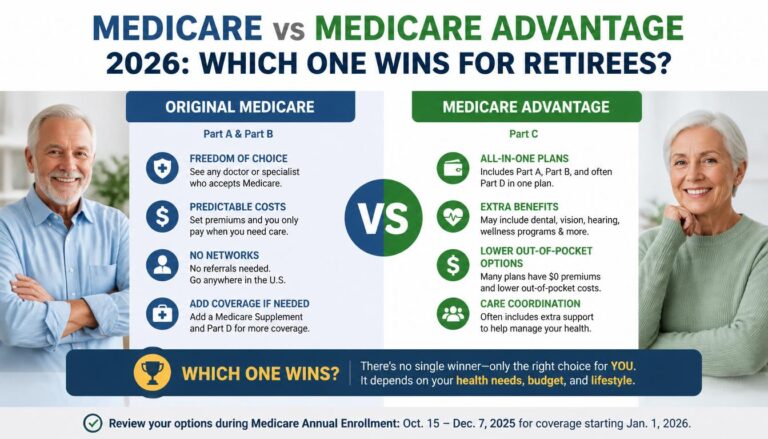

Medicare and Medicare Advantage in 2026: For the 65+ Crowd

If you’re on Medicare (Original Parts A and B), 2026 brings goodies. Part D drug cap is $2,100 out-of-pocket max—once hit, drugs are free for the year. Medicare Advantage (Part C) plans from Aetna, UnitedHealthcare, and Devoted Health top lists for networks and extras like dental, vision, hearing, and even gym memberships.

Humana and Aetna lead in ratings. Average Advantage premiums dipped slightly to about $11.50/month. Zero-premium plans are everywhere, but read the fine print—networks can shrink.

Humor alert: Medicare Advantage is like all-you-can-eat buffet insurance. Great until you realize the “extra benefits” don’t include covering that one med your doctor swears by. Shop during October 15–December 7 enrollment.

Medicaid and Other Options

Low-income? Medicaid (or CHIP for kids) covers millions with little to no cost. Eligibility varies by state—check your state’s site. Veterans: VA benefits. Short-term plans or association plans fill gaps but skip the ACA protections.

Factors to Consider When Choosing a Plan

- Your Doctors and Hospitals: In-network = cheaper.

- Prescriptions: Does your plan’s formulary cover your meds?

- Expected Medical Needs: Frequent visits? Go Gold. Rare? Bronze.

- Budget: Total cost = premium + deductible + copays.

- Out-of-Pocket Max: Caps your yearly spending—aim under $9,000 for individuals.

Make a list of your top three priorities. It’s like dating: chemistry (coverage) matters more than looks (flashy ads).

How to Compare Plans: A Step-by-Step Guide

Step 1: Log into HealthCare.gov or your state exchange. Step 2: Enter ZIP, household size, income, current doctors, and meds. Step 3: Filter by metal tier and plan type. Step 4: Use the “Summary of Benefits” PDF—read it like your life depends on it (it might). Step 5: Calculate worst-case scenario: “What if I need surgery?” Step 6: Enroll before deadlines!

Tools like the marketplace’s side-by-side comparison are gold.

Common Mistakes to Avoid (And the Funny Ones We’ve All Made)

- Ignoring networks: “My doctor’s in-network… wait, he switched?” Ouch.

- Picking cheapest premium only: Like buying a cheap car that breaks down constantly.

- Forgetting subsidies: Many qualify but don’t apply—free money, people!

- Skipping preventive care: It’s free—use it or lose it (and your health).

One classic: A friend enrolled in a “great” plan, then learned his allergy shots cost $500 because they were out-of-network. Lesson? Double-check everything.

State-Specific Tips and Future Outlook

California and New York have robust state marketplaces with extra protections. Texas and Florida? More insurer options but shop hard for value. Rural states lean on BCBS.

Looking ahead to 2027: Expect shorter open enrollment again and possible more tweaks. Premiums may rise 5-10% nationally, but competition helps.

Wrapping It Up: Your 2026 Health Insurance Game Plan

Health insurance in 2026 isn’t perfect, but with Kaiser leading the pack for value, BCBS owning networks, and smart tools on your side, you’ve got options. Don’t treat it like a chore—think of it as investing in your future self who won’t panic over bills. Take 30 minutes today to review your plan or shop if needed. Your wallet (and sanity) will thank you.