Hey there, fellow American navigating the wild world of health insurance. If you’re staring at your computer screen right now, trying to figure out what the heck to pick for 2026, you’re not alone. Picking a health plan feels a lot like choosing a spouse—you want someone reliable who won’t leave you broke when things get serious, but the options can make your head spin. With premiums climbing thanks to rising medical costs and some big changes in subsidies, it’s more important than ever to get this right. This guide breaks it all down in plain English, with a few laughs along the way, because let’s face it: if we can’t joke about surprise medical bills, what can we joke about?

I’m no insurance guru with a fancy degree—just someone who’s dug through the numbers, talked to real folks, and learned the hard way that a cheap premium doesn’t always mean cheap care. By the end of this, you’ll know exactly what to look for, who the top players are, and how to avoid the classic traps that leave people crying over their deductibles. Let’s dive in.

Why Health Insurance Still Matters in 2026 (Even If It Feels Like a Rip-Off)

Picture this: You trip over your kid’s Lego, break your ankle, and suddenly you’re staring at a $15,000 hospital bill. Without insurance, that’s not just painful—it’s life-changing. In 2026, healthcare costs keep climbing because of everything from fancy new drugs to hospital bills that seem designed by cartoon villains. Employer plans for a family of four can run around $25,000 a year total, with you chipping in maybe $6,000 or more out of your paycheck. Marketplace plans? They jumped about 18 to 26 percent on average this year after those extra COVID-era subsidies faded away.

But here’s the good news: insurance still protects you from the worst. It covers preventive stuff like check-ups and vaccines for free, handles pre-existing conditions without kicking you to the curb, and caps your out-of-pocket spending so one bad year doesn’t bankrupt you. Plus, with over 20 million people still using the ACA Marketplace, it’s clear most of us need this safety net. Skipping coverage isn’t just risky—it’s illegal in some ways thanks to the individual mandate in certain states, and it could mess with your taxes. So yeah, even if it feels like paying for peace of mind you hope you never use, it’s worth it. Think of it as your financial seatbelt.

Understanding the Basics: What Even Is Health Insurance, Anyway?

Let’s keep this simple because insurance companies love throwing around terms like they’re speaking another language. At its core, health insurance is a deal you make with a company: You pay a monthly premium (like a subscription fee), and in return, they help cover your doctor visits, hospital stays, prescriptions, and more when you get sick or hurt.

There are two big buckets of costs. First, the premium—that’s what you pay every month no matter what. Second are the costs when you actually use care: deductibles (the amount you pay before insurance kicks in), copays (fixed fees like $30 for a doctor visit), and coinsurance (your percentage of the bill, say 20 percent). Then there’s the out-of-pocket maximum, which is the most you’ll ever pay in a year before insurance covers 100 percent. Hit that cap, and you’re done paying for the year—thank goodness.

In 2026, one cool tweak is that all Bronze and Catastrophic plans now work with Health Savings Accounts (HSAs). That means you can stash pre-tax dollars to pay for stuff like deductibles. It’s like the government giving you a little high-five for being smart with your money. But remember, not everyone qualifies for subsidies anymore at the same level. Those enhanced tax credits from the pandemic? They expired at the end of 2025, so many folks are seeing higher monthly bills even if they stay with the same plan.

Types of Health Insurance Plans: Sorting Through the Alphabet Soup

Health plans come in different flavors, and picking the wrong one is like ordering a spicy meal when you can’t handle heat—it’s going to hurt later. Here’s the breakdown:

- HMO (Health Maintenance Organization): These are usually the cheapest. You pick a primary care doctor who acts like the boss of your care. Need a specialist? Get a referral first. Everything stays in-network, or you pay full price (except emergencies). Great if you don’t mind sticking close to home and want low premiums and copays. Downside? Less flexibility. Kaiser Permanente loves HMOs and often tops charts because their doctors and hospitals work together like a well-oiled machine.

- PPO (Preferred Provider Organization): The flexible friend. No referrals needed, and you can see out-of-network doctors (though it costs more). Perfect for families who travel or have specialists scattered around. Blue Cross Blue Shield often shines here with massive networks. Expect higher premiums, but the freedom feels worth it when your kid needs that one pediatrician across town.

- EPO (Exclusive Provider Organization): A middle child between HMO and PPO. No referrals, but you’re stuck in-network like an HMO. No out-of-network coverage except emergencies. Good balance if you want options without the full PPO price tag.

- POS (Point of Service): Rare these days, but it mixes HMO rules with some PPO flexibility. You pay more for out-of-network.

- HDHP (High-Deductible Health Plan): Paired with an HSA, these have low premiums but sky-high deductibles (think $1,500+ before insurance helps much). Ideal for healthy people who rarely go to the doctor. In 2026, they’re even more popular since Bronze plans now qualify for HSAs.

Here’s a quick comparison table to make it visual:

| Plan Type | Monthly Premium | Deductible | Referrals Needed? | Out-of-Network Coverage? | Best For |

|---|---|---|---|---|---|

| HMO | Lowest | Lower | Yes | No (except emergencies) | Budget-conscious, routine care |

| PPO | Highest | Higher | No | Yes (higher cost) | Flexibility, families |

| EPO | Moderate | Moderate | No | No (except emergencies) | Balance seekers |

| HDHP | Low | Very High | Varies | Varies | Healthy folks with HSAs |

Key Factors to Consider When Choosing a Plan: Don’t Get Caught Off Guard

Buying insurance without checking these is like buying a car without looking under the hood. First, network size. Does your doctor or hospital take the plan? Use the insurer’s website tool to check—nothing ruins your day like finding out your favorite doc is “out of network” and suddenly costs double. Kaiser Permanente wins here in many states because everything is in-house.

Next, costs. Look at the full picture: premium + deductible + out-of-pocket max. A $200 monthly plan with a $8,000 deductible might save you now but bankrupt you later. Silver plans are the sweet spot for most because subsidies often make them affordable, and they balance costs well.

Coverage details matter too. Does it cover your prescriptions? Mental health? Maternity? Dental or vision? In 2026, essential health benefits are still required, but some extras like certain gender-affirming care might not be mandatory in every plan anymore. Read the fine print or you’ll be that person calling customer service in tears.

Customer service and ratings. Nobody wants to wait on hold for an hour when they’re sick. Kaiser scored 4.42 stars in big surveys for 2026—top spot six years running—thanks to easy payments and happy customers. Check complaint ratios on sites like the NAIC.

Finally, your health and life stage. Young and healthy? Bronze might work. Family with kids? Gold for lower copays on all those pediatric visits. Chronic conditions? Prioritize low out-of-pocket maxes.

Best Overall Health Insurance Plans in 2026

If I had to crown winners, Kaiser Permanente takes the top spot again in 2026. They earned the highest marks from Insure.com and Forbes for customer satisfaction, affordability, and quality care. Their integrated model—doctors, hospitals, and pharmacies all under one roof—means fewer hassles and better coordination. Premiums average around $580-$600 for a Silver plan before discounts, and folks rave about the app and quick appointments. The only catch? They’re not everywhere—mainly West Coast, plus some spots in the East and South.

Blue Cross Blue Shield comes in hot for nationwide coverage. With local plans in every state, their networks are huge, making them ideal if you move around or need options. They often rank best for PPO shoppers and families, with solid ratings around 4.0+ stars. Expect a bit higher premiums, but the peace of mind is real.

UnitedHealthcare shines for employer plans and folks who want global travel coverage. Their networks are massive, and they’re great if you’re self-employed or switching jobs. Aetna and Humana round out the top tier, especially for customizable options and Medicare tie-ins.

Here’s a simple list of standout companies:

- Kaiser Permanente: Best overall, integrated care king.

- BCBS: Best networks, family favorite.

- UnitedHealthcare: Best for big employers and flexibility.

- Oscar: Tech-savvy with great apps and member experience.

- Ambetter (Centene): Affordable for lower-income folks.

Best Health Insurance for Families in 2026

Families need plans that handle everything from soccer injuries to annual check-ups without breaking the bank on copays. Blue Cross Blue Shield often wins here because of their huge provider lists—your pediatrician, OB-GYN, and orthopedist are probably in-network. Many BCBS plans offer low copays for kids’ visits and maternity coverage that feels like a hug.

UnitedHealthcare is another family hero with simplified structures and massive networks (over 1.3 million providers). They have family-friendly extras like telehealth that saves you a trip when the kids have the sniffles.

For affordability, look at Anthem or Ambetter. A family Silver plan might run $1,200-$2,000 a month before subsidies, but tax credits can slash that. Pro tip: Choose a plan with a lower out-of-pocket max if your kids are accident-prone—trust me, one ER visit per kid per year adds up.

Humor break: Raising kids is expensive enough without insurance turning every ear infection into a second mortgage.

Best Plans for Young Adults and Individuals

If you’re under 30 or single with no kids, you’re probably healthy and don’t want to overpay. Kaiser Permanente or Molina often offer the lowest rates for individuals—think $500-$600 a month for Silver before help. Catastrophic plans are back in play for young folks who qualify, with super-low premiums but high deductibles. Pair it with an HSA, and you’re basically saving for a rainy day (or a broken arm).

Oscar gets props for young people because their app is slick, like having a virtual assistant who reminds you about refills. Avoid over-insuring—Bronze plans keep costs low if you’re the “I only go to the doctor when I’m dying” type.

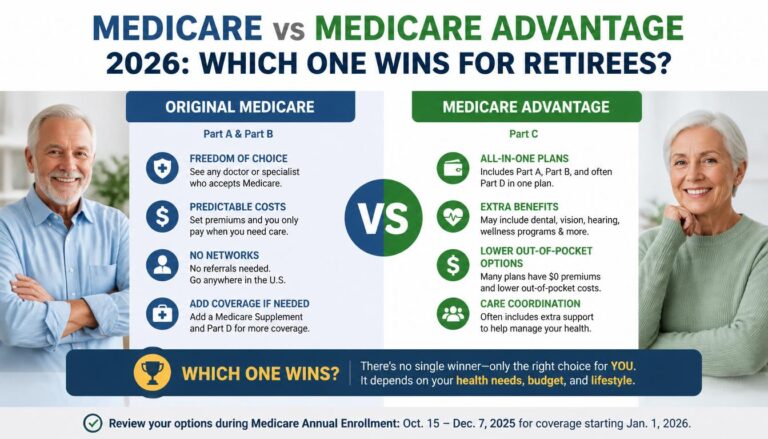

Best Options for Seniors: Medicare in 2026

Turning 65? Medicare is your new best friend. Original Medicare (Parts A and B) covers hospital and doctor stuff, but most folks add a Medicare Advantage plan for extras like dental, vision, and gym memberships.

Aetna Medicare and Devoted Health topped U.S. News rankings for 2026 thanks to strong ratings in screenings and care coordination. UnitedHealthcare and Humana offer tons of $0-premium plans—86 percent of folks picked one this year. Average Advantage premium sits around $14 a month, but watch out-of-pocket maxes, which crept up a bit.

Part D for drugs? Humana and Centene lead the pack. Shop during Medicare’s open enrollment (October 15 to December 7) or you’ll pay penalties. Funny note: Medicare feels like the government finally giving you a gold watch after decades of working—except the watch sometimes needs batteries (extra coverage).

Employer-Sponsored Plans vs. Individual Marketplace: Which One Wins?

If your job offers insurance, grab it—employers often cover 70-80 percent of the premium, making it cheaper than going solo. In 2026, these plans are seeing increases too, but the group rate beats individual shopping. Open enrollment at work is usually in the fall.

No job coverage? Head to HealthCare.gov (or your state’s marketplace). You can browse 2026 plans now and see estimated prices. Subsidies still exist, but they’re less generous—expect to pay more out of pocket. The average subsidized lowest-cost plan is about $50 a month after credits, but that jumps if your income is higher. Enrollment dropped over a million people this year because of the changes, so don’t wait.

How to Enroll and Score the Best Deal: Pro Tips That Actually Work

Step one: Know your open enrollment window. For Marketplace, it’s usually November 1 to January 15 in most states. Miss it, and you’re stuck unless you have a qualifying life event like getting married or losing a job.

Step two: Use the preview tool on HealthCare.gov to window-shop plans and prices before applying. Plug in your ZIP code, income, and household size.

Step three: Compare at least three plans side-by-side. Look for your doctors, meds, and total estimated costs (not just premium).

Step four: Apply for subsidies if eligible— even if you think you make too much, the calculator might surprise you.

Bonus tip: Call your doctor’s office and ask, “Do you take Plan X in 2026?” Do this before you sign. And read reviews—real people spill the tea on forums about claim denials.

Common Pitfalls to Avoid (And the Funny Ways They Bite You)

One big oops: Ignoring the network. You switch jobs, keep your old plan, and bam—your specialist costs $500 a visit. Another: Picking the cheapest premium without checking the deductible. It’s like buying a cheap phone that dies after six months.

Forgetting to update income? You could owe money back at tax time. And don’t sleep on preventive care—it’s free and catches stuff early, saving you thousands (and awkward conversations with your doctor).

Humor alert: The worst is assuming “it’ll never happen to me” until it does, and then you’re googling “how to sell a kidney on eBay.”

State-by-State Twists: Because Nothing in America Is Simple

Insurance is regulated by states, so what’s great in California (hello, Kaiser) might stink in Texas. Check your state’s marketplace or department of insurance website for local heroes. For example, Ambetter and Oscar score high in Texas for 2026 affordability. Always verify networks locally—national rankings are a starting point, not gospel.

Looking Ahead: What’s Next After 2026?

Costs will probably keep rising, but tech like telehealth and AI might help. Watch for any new laws on subsidies or drug prices. The smart move? Review your plan every year during open enrollment. Life changes fast—new baby, new job, new health issue—and so should your coverage.

Wrapping It Up: Your 2026 Insurance Game Plan

Choosing health insurance in 2026 doesn’t have to feel like a root canal. Focus on Kaiser or BCBS if you want reliability, match the plan type to your lifestyle, and always calculate the full-year costs. Shop smart, ask questions, and remember: the best plan is the one that keeps you healthy without draining your wallet dry.

You’ve got this. Take a deep breath, grab a coffee, and start comparing plans today. Your future self (and your bank account) will thank you. And if you end up with a plan that actually works without drama? That’s worth celebrating—maybe with a donut, because hey, preventive care includes treating yourself once in a while.